How much has your State Farm premium changed because of wildfire risk?

Getting an affordable homeowners insurance policy in California is becoming harder and harder, especially in areas with higher wildfire risk. Homes near undeveloped wildland vegetation, nearly a third of California homes, are at greater risk of burning and face much higher premiums for fire coverage or an inability to secure coverage at all.

Insurers have long requested, and may soon be allowed, to use wildfire catastrophe models to set overall rates. But many companies, including State Farm, Farmers and Allstate, already use these models to adjust their rates based on location. An L.A. Times analysis of State Farm rate filings shows how these models have resulted in dramatic increases in rates for vulnerable areas in the past four years.

The Times’ analysis of rate filings submitted to the California Department of Insurance show that State Farm's uses a location rating factor, a number that is generated using wildfire models, multiplied to the base rate as part of its premium calculation.

In many places this number has been rising. Since 2020, some areas in the hills east of San Diego have seen the biggest increase, with their factor nearly tripling and pushing premiums above $20,000 before deductions.

Enter an address or click on the map below to see how location rating factors have impacted rates in your location

When asked about its use of wildfire models to generate the location rating factor, otherwise known as segmentation, State Farm said its rate changes are "driven by increased costs" and that customers with questions should speak to their local agent.

The Department of Insurance is aware that the process is opaque. Department spokesperson Michael Soller says “People do not know what their risk score is. They don't know what goes into the risk score. It's a black box. Yet, the risk score can be used to [charge you] double what somebody else pays.”

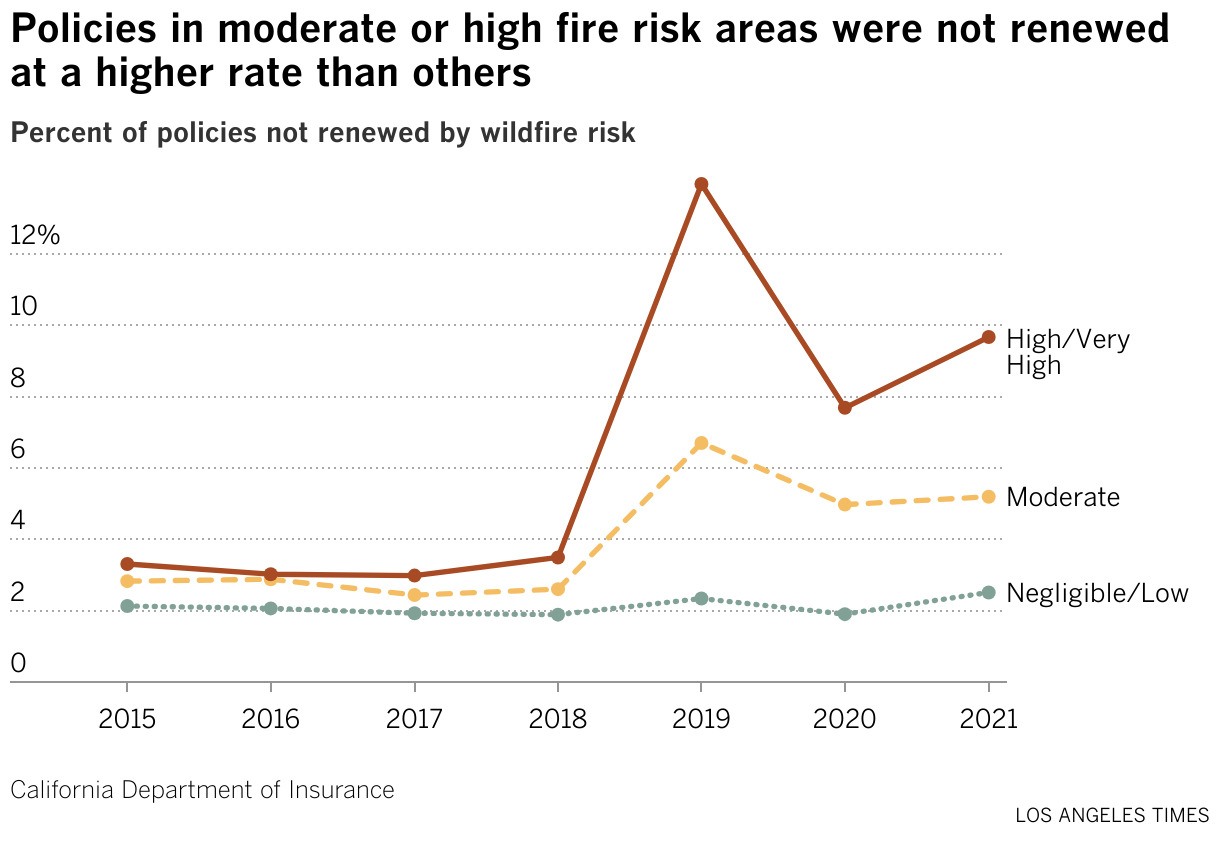

Insurers are allowed to use wildfire models to determine where to write policies. As a result, many of the areas facing high rates due to the location rating factor are also at a greater risk of nonrenewal. In recent years, nonrenewals disproportionately hit high-risk areas harder.

Under Insurance Commissioner Ricardo Lara’s new policy, model results could also be incorporated directly into the overall rate. Critics of this proposed plan argue that there is not enough public transparency into how the models work. They are concerned that they could be used to justify unnecessary rate hikes.

But the companies say they cannot survive on the current rate system.

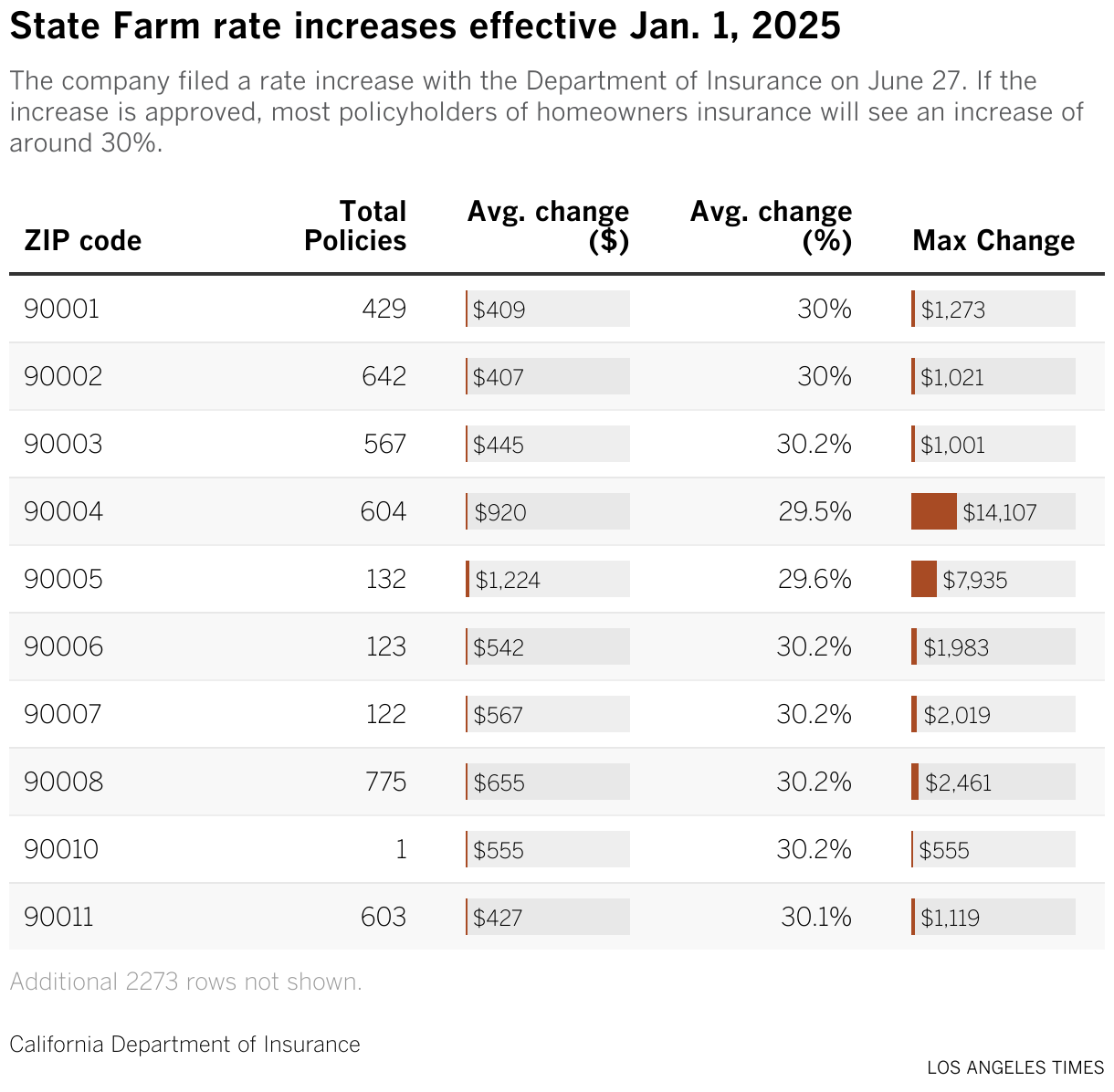

In its most recent rate filing, State Farm requested a 30% overall rate increase, its biggest increase ever. Unlike previous rate increases which tend to have much higher rates for wildfire risk areas, increases are between 21-31% in all ZIP Codes.

Search in the table below to see how State Farm’s proposed rate increase will impact your ZIP Code